Prime Minister Modi in 2016 highlighted the Reserve Bank of India’s (RBI’s) role in achieving the vision of a developed India (“Viksit Bharat”). This includes ensuring financial stability, credit access for all (from small vendors to big businesses) and fostering public trust in the banking system.

Tag: GS – 3 Banking Sector & NBFCs – Monetary Policy- Inclusive Growth

For Prelims: Reserve Bank of India Act, 1934, Prompt Corrective Action (PCA) Framework, Non-performing assets (NPAs), Consumer Price Index (CPI), Non-Banking Financial Companies (NBFCs), Financial Stability and Development Council (FSDC), Raghuram Rajan committee (2008), Nachiket Mor Committee, P.J. Nayak Committee.

For Mains: Key Achievements and Challenges of the Reserve Bank of India.

Contents

- 1 Context:

- 2 UPSC Civil Services Examination, Previous Year Questions (PYQs)

- 3 FAQs on 90 Years of RBI and “Viksit Bharat” Vision

- 3.1 1. What is “Viksit Bharat” and how does RBI play a role?

- 3.2 2. How has the RBI contributed to managing public debt?

- 3.3 3. What are some initiatives by the RBI promoting financial inclusion?

- 3.4 4. How does the RBI’s monetary policy impact “Viksit Bharat”?

- 3.5 5. What are some future challenges for the RBI in achieving Vikasit Bharat’s vision?

- 4 In case you still have your doubts, contact us on 9811333901.

Context:

- The Prime Minister addressed the opening ceremony of RBI@90, marking 90 years of the Reserve Bank of India (RBI) in Mumbai, Maharashtra.

- The Prime Minister also released a commemorative coin to celebrate this milestone, as RBI commenced its operations on April 1, 1935.

Establishment of the Reserve Bank of India (RBI):

- Enactment of the RBI Act: The Reserve Bank of India Act was passed by the British government in 1934.

- Establishment of RBI: The RBI was officially formed in Calcutta (now Kolkata) on April 1, 1935.

- Basis of Establishment: The establishment of the RBI was based on the recommendations of the Royal Commission on Indian Currency & Finance in 1926, also known as the Hilton Young Commission.

- Influence of Dr. Ambedkar: The concept of the RBI was influenced by the strategies outlined by Dr. Ambedkar in his book “The Problem of the Rupee – Its Origin and Its Solution.”

- Nationalisation in 1949: Prior to 1949, the RBI was owned by private stakeholders; it was nationalised in 1949.

- First Governor: Sir Osborne Smith served as the first Governor of the RBI.

- First Indian Governor: C.D. Deshmukh became the first Indian Governor of the RBI.

Objectives:

- The Preamble of the RBI outlines the fundamental functions of the Reserve Bank:

- Regulating the issuance of banknotes and maintaining reserves to ensure monetary stability in India, as well as managing the currency and credit system for the country’s benefit.

- Establishing a modern monetary policy framework capable of addressing the complexities of the evolving economy.

- Striving to maintain price stability while also promoting growth objectives.

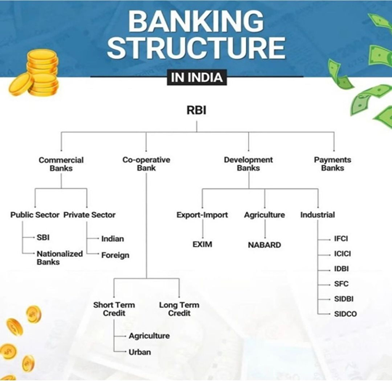

Structure of RBI:

- The Reserve Bank’s operations are overseen by a central board of directors.

- These directors are appointed by the Government of India in accordance with the Reserve Bank of India Act.

- Directors serve for a term of four years, either appointed or nominated.

Acts Administered by the RBI:

- Reserve Bank of India Act, 1934

- Public Debt Act, 1944/Government Securities Act, 2006

- Government Securities Regulations, 2007

- Banking Regulation Act, 1949

- Foreign Exchange Management Act, 1999

- Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (Chapter II)

- Credit Information Companies (Regulation) Act, 2005

- Payment and Settlement Systems Act, 2007

- Payment and Settlement Systems Act, 2007 As Amended up to 2019

- Payment and Settlement Systems Regulations, 2008 As Amended up to 2022

- Factoring Regulation Act, 2011

Functions of RBI:

| Functions | Description |

| Issuer of Currency Notes | The system followed by RBI for the issue of currency notes is known as the Minimum Reserve System. Under the Minimum Reserve System, the RBI is required to hold a minimum reserve of gold and foreign securities equivalent to ₹200 crore, of which at least ₹115 crore should be in the form of gold. The RBI can issue currency notes beyond this minimum reserve based on its requirements and the needs of the economy. The currency notes issued by the RBI are liabilities of the RBI and are backed by the assets held in the form of gold and foreign securities. The RBI has the authority to issue and withdraw currency notes from circulation as per the needs of the economy. |

| Banker to other Banks | The Central Bank acts as a custodian of the cash reserves of commercial banks. Banks of the country are required to keep a certain percentage of their deposits with the Central Bank (known as Cash Reserve Ratio). As a lender of last resort, the Central Bank extends loans to commercial banks when all other sources of raising funds are practically closed. It acts as a bank for central clearance, settlements, and transfers. As all commercial banks have accounts with the Central Bank, they can easily settle claims of various commercial banks against each other by making debit and credit entries in their accounts. |

| Banker to the Government | The RBI Act of 1934 mandates that the Central Government must delegate all its financial operations, including money management, remittance, exchange, and banking transactions within India, to the Reserve Bank. Additionally, the Reserve Bank has the authority to serve as a banker to State Governments through mutual agreements. As a banker to the Government, the Reserve Bank receives and pays money on behalf of the various Government Departments. It provides Ways and Means Advances, a short-term interest-bearing advance to the Governments to meet temporary mismatches in their receipts and payments. Besides, like a portfolio manager, it also arranges for the investment of surplus cash balances of the Government. |

| Foreign Exchange Management | Custodian: The RBI serves as the custodian of the country’s foreign exchange reserves. Exchange Control: The RBI regulates the forex market through stringent exchange control regulations. Banks are not allowed to purchase dollars from the RBI for speculative purposes in the interbank market. The central bank prohibits the sale of these dollars in the overseas cross-currency market. Managing Currency Volatility: RBI intervenes in the forex market to mitigate currency volatility, especially in the dollar/rupee exchange rate. Through agreements with other banks, the RBI takes measures to stabilise currency fluctuations and maintain market confidence. |

| Credit control | It regulates the credit creation capacity of commercial banks by using various credit control tools. The primary objective is to control inflationary tendencies present in the economy to ensure high economic growth with an adequate level of liquidity and maximum utilisation of resources. |

| Supervisory Function | It has the power to issue licences for setting up new banks, opening new branches, deciding minimum reserves, inspecting the functioning of commercial banks in India and abroad, and guiding and directing commercial banks in India. It can have periodical inspections and audit of the commercial banks in India |

| Promotional Functions of RBI | Development of Agriculture: In an agrarian economy like ours, the RBI must pay special attention to the credit needs of agriculture and allied activities. Provision of Industrial Finance: In this regard, the RBI has always been instrumental in setting up special financial institutions such as ICICI Ltd. IDBI, SIDBI, EXIM BANK, etc. Provisions of Training: The RBI has always tried to provide essential training to the banking industry’s staff. The RBI has set up bankers’ training colleges in several places. Collection of Data: Being the apex monetary authority of the country, the RBI collects, processes and disseminates statistical data on several topics. It includes interest rate, inflation, savings and investments etc. Publication of the Reports: The RBI regularly publishes reports and bulletins, including weekly reports, the annual Report, and the Report on Trend and Progress of Commercial Banks India. Promotion of Banking Habits: It has established many institutions, such as the Deposit Insurance Corporation (1962), UTI (1964), IDBI (1964), NABARD (1982), and NHB (1988). These organisations develop and promote banking habits among the people. Promotion of Export through Refinance: The Export-Import Bank of India (EXIM Bank India) and the Export Credit Guarantee Corporation of India (ECGC) are supported by refinancing their lending for export purposes. |

Challenges Encountered by the Reserve Bank of India (RBI):

- Autonomy of RBI:

- The Reserve Bank’s autonomy is not legally mandated, as Section 7 of the RBI Act allows the central government to issue directions to the RBI in the public interest.

- Instances of government influence over RBI’s decision-making, especially concerning monetary policy, regulatory actions, and reserve utilisation, have raised concerns about its autonomy.

- Inflation Management:

- Despite implementing a flexible inflation-targeting framework, the RBI faces challenges in controlling inflation.

- Food inflation, a significant component of the Consumer Price Index (CPI), surged to 9.53% in December 2023, posing hurdles due to India’s complex economic structure, supply-side constraints, and external factors like global commodity prices.

- Writing off Loans without Adequate Recovery:

- Banks write off loans to lower Gross Non-performing Assets (GNPA) to a 10-year low of 3.9% of advances in March 2023. While addressing short-term balance sheet concerns, this practice raises transparency issues and fails to resolve underlying causes of NPAs.

- Financial Stability and Systemic Risks:

- Ensuring financial stability amid rapid credit growth, interconnectivity among financial institutions, and vulnerabilities in segments like shadow banking remains challenging.

- Episodes such as the YES Bank and Infrastructure Leasing & Financial Services Ltd crises highlight the need for improved oversight.

- Incomplete Transmission of Monetary Policy:

- Monetary policy easing by the RBI has not translated into lower lending rates by banks due to rigidities, liquidity conditions, and risk perceptions. Ineffective transmission limits the impact of RBI’s policy measures on the economy.

- Digitalization and Cybersecurity:

- Technological advancements in banking outpace regulatory frameworks, posing challenges in compliance with cybersecurity standards and data protection regulations.

- Cyber threats like hacking and phishing undermine financial infrastructure integrity, as evidenced by the recent Paytm crisis.

- Financial Inclusion and Access to Credit:

- Despite RBI’s efforts, access to credit remains a challenge, particularly for small and marginalised borrowers, due to inadequate bank branches and digital infrastructure in rural areas.

- Growth in the rural digital payments market will more than triple from USD 3 trillion to USD 10 trillion by 2026 but requires improved internet connectivity and banking infrastructure.

Strategies to Improve the Functioning of the Reserve Bank of India (RBI):

- Strengthening Regulatory Framework:

- Enhance regulatory frameworks for robust supervision and regulation of banks and financial institutions, with periodic reviews to adapt to market dynamics and emerging risks.

- Utilise recommendations from committees like the Raghuram Rajan committee (2008) to establish the Financial Stability and Development Council (FSDC) for enhanced financial stability and regulatory coordination.

- Enhancing Financial Inclusion:

- Implement measures to expand access to banking services, promote digital payments, and support initiatives reaching underserved populations and regions.

- Follow recommendations from committees such as the Nachiket Mor Committee (2014) for phased approaches to achieve universal financial inclusion through innovative delivery mechanisms.

- Improving Monetary Policy Transmission:

- Address bottlenecks in monetary policy transmission mechanisms to ensure effective influence of policy rate changes on lending and borrowing rates, facilitating credit flow to productive sectors.

- Utilise measures like the Marginal Cost of Funds based Lending Rate (MCLR) introduced by the RBI to enhance policy rate transmission.

- Enhancing Risk Management Practices:

- Strengthen risk management frameworks within banks and financial institutions to identify, assess, and mitigate various risks, including credit, liquidity, operational, and cyber risks.

- Implement initiatives like the Insolvency and Bankruptcy Code (IBC) framework to resolve issues such as bad loans and promote healthy credit growth.

- Promoting Technological Innovation:

- Encourage technological innovation and adoption within the financial sector while ensuring data security and consumer protection.

- Utilise initiatives like the Regulatory Sandbox (RS) ecosystem established by the RBI to systematically expand the FinTech ecosystem in India.

- Increasing Transparency and Communication:

- Enhance transparency and communication channels between the RBI, financial institutions, and the public to improve understanding of monetary policy decisions and regulatory changes.

- Utilise platforms like the RBI Governor’s bi-monthly monetary policy statement and press conferences for clarity on policy decisions and outlook.

- Capacity Building and Training:

- Invest in capacity building and training programs for RBI staff and stakeholders to enhance skills, knowledge, and expertise in financial regulation, supervision, monetary policy, and emerging technologies.

- Follow recommendations like those from the Damodaran Committee (2011) on enhancing training programs for bank employees to improve customer service.

- Strengthening Governance and Accountability:

- Implement measures to enhance governance structures, accountability mechanisms, and internal controls within the RBI to ensure effective decision-making, transparency, and integrity.

- Utilise recommendations from committees like the P.J. Nayak Committee (2014) to enhance the autonomy and governance of public sector banks.

- Collaboration and Coordination:

- Foster collaboration and coordination with other regulatory authorities, government agencies, international organisations, and stakeholders to address cross-cutting issues and promote financial stability.

- Participate actively in international forums like the Financial Stability Board (FSB) and the Bank for International Settlements (BIS) to exchange information and coordinate policy efforts.

UPSC Civil Services Examination, Previous Year Questions (PYQs)

Prelims

Q:1 Which of the following statements is/are correct regarding the Monetary Policy Committee (MPC)? (2017)

- It decides the RBI’s benchmark interest rates.

- It is a 12-member body including the Governor of RBI and is reconstituted every year.

- It functions under the chairmanship of the Union Finance Minister.

Select the correct answer using the code given below:

(a) 1 only

(b) 1 and 2 only

(c) 3 only

(d) 2 and 3 only

Ans: A

Q:2 If the RBI decides to adopt an expansionist monetary policy, which of the following would it not do? (2020)

- Cut and optimise the Statutory Liquidity Ratio

- Increase the Marginal Standing Facility Rate

- Cut the Bank Rate and Repo Rate

Select the correct answer using the code given below:

(a) 1 and 2 only

(b) 2 only

(c) 1 and 3 only

(d) 1, 2 and 3

Ans: B

Mains

Q:1 The product diversification of financial institutions and insurance companies, resulting in overlapping of products and services strengthens the case for the merger of the two regulatory agencies, namely SEBI and IRDA. Justify. (2013)

FAQs on 90 Years of RBI and “Viksit Bharat” Vision

1. What is “Viksit Bharat” and how does RBI play a role?

- Answer: “Viksit Bharat” translates to “Developed India.” The RBI’s role is to establish a robust banking system that facilitates financial inclusion and economic growth across all regions of India, especially underserved areas. This aligns with Vikasit Bharat’s vision of an inclusive and prosperous nation.

2. How has the RBI contributed to managing public debt?

- Answer: The RBI has a successful track record in managing public debt. It issues government loans at competitive rates, enabling infrastructure development and public sector expansion. Additionally, it provides the government with short-term financial assistance.

3. What are some initiatives by the RBI promoting financial inclusion?

- Answer: We don’t have specific details here, but the RBI likely implements initiatives like promoting microfinance, simplifying account opening procedures, and expanding the reach of digital banking solutions. These initiatives aim to bring more people into the formal financial sector.

4. How does the RBI’s monetary policy impact “Viksit Bharat”?

- Answer: The RBI’s monetary policy tools like interest rates and reserve ratios influence credit availability and economic activity. By calibrating these policies, the RBI can encourage lending to underserved sectors and promote inclusive growth, contributing to Vikasit Bharat’s goals.

5. What are some future challenges for the RBI in achieving Vikasit Bharat’s vision?

- Answer: Challenges might include ensuring financial literacy reaches all corners of the country, bridging the digital divide for online banking access, and addressing potential risks associated with financial inclusion. The RBI will likely strategize to overcome these hurdles.

In case you still have your doubts, contact us on 9811333901.

For UPSC Prelims Resources, Click here

For Daily Updates and Study Material:

Join our Telegram Channel – Edukemy for IAS

- 1. Learn through Videos – here

- 2. Be Exam Ready by Practicing Daily MCQs – here

- 3. Daily Newsletter – Get all your Current Affairs Covered – here

- 4. Mains Answer Writing Practice – here