HomeUPSC MainsUPSC Mains – What is your understanding of Non-Performing Assets (NPA)? Despite various measures taken by the Government of India, the banking sector in India continues to grapple with the persistent challenge of Non-Performing Assets. Examine. (15M, 250 words)

UPSC Mains – What is your understanding of Non-Performing Assets (NPA)? Despite various measures taken by the Government of India, the banking sector in India continues to grapple with the persistent challenge of Non-Performing Assets. Examine. (15M, 250 words)

Non-performing assets (NPAs) refer to loans or advances where principal or interest payments remain overdue for 90 days or more. Despite a decrease from 11.5% in 2018 to 3.9% in FY 2023, NPAs remain a significant concern in the banking sector.

Body:

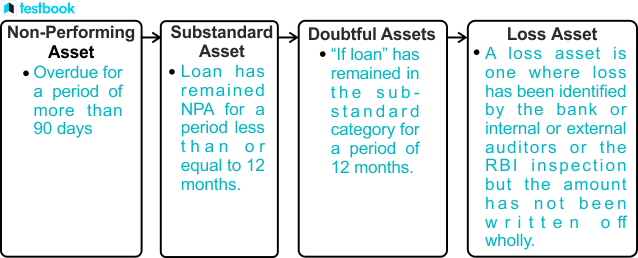

Non-Performing Asset (NPA) Classification:

Reasons for the Persistence of the NPA Crisis in the Indian Banking Sector:

Slow NPA Resolution: Merely 484 out of 4,376 cases under the Insolvency and Bankruptcy Code (IBC) have been resolved, indicating a substantial backlog in unresolved cases.

Sector-Specific Challenges: Sectors like power, with NPAs amounting to ₹1.02 lakh crore ($14 billion) as of March 2021, pose hurdles to overall resolution efforts.

Economic Slowdown and Pandemic Impact: The pandemic and economic slowdown have contributed to an increase in gross NPAs, projected to reach 9.8% by March 2022.

Governance and Regulatory Issues: Weak corporate governance practices and lax regulatory oversight have exacerbated the NPA crisis.

Evergreening of Loans: Practices like evergreening perpetuate the NPA problem.

Actions Taken by the Government of India:

Recognition of NPAs: Asset Quality Review (AQR) in 2015 and Credit Information Bureau (India) Ltd. (CIBIL) establishment in 2000 to prevent NPAs.

Resolution and Recovery: Implementation of Insolvency and Bankruptcy Code (IBC), Asset Reconstruction Companies (ARCs), and the SARFAESI Act.

Recapitalization of Public Sector Banks (PSBs): PSBs received a recapitalization of Rs. 3.12 lakh crore over the past four financial years.

Reforms in PSBs and Financial Ecosystem: Board-approved loan policies, third-party data sources for due diligence, and specialized monitoring agencies for effective oversight.

Way Forward:

Establishment of a Bad Bank to manage NPAs, allowing banks to focus on core lending activities.

Implementation of Nayak Committee recommendations, including Bank Board Bureau’s role in appointments and reducing government stake in PSBs.

Enhanced credit appraisal, penalties for wrongdoing, and strengthening RBI governance and regulation.

Diagnostics for willful default and prevention of evergreening of loans through penalties and accountability measures.

In case you still have your doubts, contact us on 9811333901.

")