Welcome to the Ministry of Finance, the cornerstone of economic policy and financial management within our government. Our mission is to ensure fiscal stability, promote sustainable growth, and facilitate equitable distribution of resources. With a commitment to transparency and accountability, we strive to optimize public finances for the benefit of all citizens.

Old Pension Scheme (OPS): The Old Pension Scheme (OPS) is a significant topic with various economic and socio-political implications. Here’s a breakdown of the key points and recommendations provided:

Contents

- 0.0.1 Old Pension Scheme (OPS)

- 0.0.2 National Pension System (NPS)

- 0.0.3 Impact of OPS on Socio-Economic Landscape

- 0.0.4 Recommendations for Equitable Resource Distribution

- 0.0.5 Additional Points:

- 0.0.6 Nirbhaya Fund:

- 0.0.7 Public Financial Management System (PFMS):

- 0.0.8 Factors for the Successful Evolution of PFMS:

- 0.0.9 PAC Observations:

- 0.0.10 Conclusion:

- 0.0.11 The Atal Pension Yojana (APY)

- 1 FAQs

- 1.1 Q1. What is the role of the Ministry of Finance?

- 1.2 Q2. How does the Ministry of Finance contribute to economic development?

- 1.3 Q3. What measures does the Ministry of Finance take to ensure fiscal responsibility?

- 1.4 Q4. How does the Ministry of Finance support citizens’ financial well-being?

- 1.5 Q5. What initiatives is the Ministry of Finance undertaking to address economic challenges?

- 2 In case you still have your doubts, contact us on 9811333901.

Old Pension Scheme (OPS)

- Definition: OPS, also known as the Defined Benefit Pension System, is a retirement plan offered by the Indian government to its employees. It guarantees retired government employees a fixed monthly pension based on their final salary and years of service.

- Funding: The government funds this pension scheme, and the payments come from its current revenues. This leads to an increase in pension liabilities.

National Pension System (NPS)

- Definition: NPS is a market-linked, defined contribution pension system introduced in India in 2004 to replace the OPS. It’s designed to provide retirement income to all Indian citizens, including government employees, private sector workers, and self-employed individuals.

Impact of OPS on Socio-Economic Landscape

- Inequality and Regressive Redistribution:

- The Sixth Pay Commission increased government employees’ salaries, favoring them over the majority of the population.

- This creates a regressive redistribution mechanism benefiting the better-off class.

- Rising Pension Liabilities:

- Due to the Sixth pay matrix, pension liabilities for the government have surged, reaching 9% of total state expenditure.

- It’s projected that by 2050, pension expenses will account for 19.4% of total state spending.

- Disproportionate Burden on Lower Class:

- The bottom 50% of the population faces a higher burden of indirect taxation compared to their income.

- Supporting government employees’ pensions under OPS can potentially push them deeper into poverty.

- Expenditure Challenges and Public Goods:

- As the population ages and public services like education and healthcare become critical, OPS poses challenges for funding public goods.

- This may result in reduced spending on vital social sectors, affecting marginalized groups.

- Monopolization of Future Labor Markets:

- OPS can contribute to the monopolization of future labor markets by a specific class, strengthening bureaucratic dominance.

Recommendations for Equitable Resource Distribution

- Focus on Equitable Distribution:

- Opposition to OPS should emphasize fair distribution of resources and the expansion of universal provisions for public goods.

- Participatory Pension System:

- Implement a participatory pension system for government employees to ensure more egalitarian outcomes.

- Reform NPS for Lower-Rung Employees:

- Adjust NPS to provide a guaranteed monthly return for lower-level employees.

- Address Unequal Pay:

- Administer reforms to address wage disparities among different ranks of employees.

- Progressive Taxation and Fiscal Responsibility:

- Advocate for progressive taxation on the top 10% and rationalization of pensions for political executives to ensure fiscal responsibility.

This comprehensive analysis provides an in-depth understanding of the Old Pension Scheme and its impact on India’s socio-economic landscape, along with recommendations for a more equitable resource distribution system.

Additional Points:

- Old Pension Scheme (OPS):

- Discontinuation Year: Discontinued in 2004.

- Guaranteed Income: Guaranteed life-long income after retirement, typically equal to 50% of the most recently drawn salary

- Expenditure: The expenditure on the pension is borne by the government.

- National Pension Scheme (NPS):

- Administration: Administered by the Pension Fund Regulatory and Development Authority (PFRDA), Ministry of Finance, Government of India.

- Trust Ownership: National Pension System Trust (NPST), established by PFRDA, is the registered owner of all assets under NPS.

- Purpose: A voluntary and long-term retirement investment plan to provide old age security to Indian citizens. It offers a regulated market-based return for effective retirement planning.

- Launch Date: Launched in January 2004 initially for government employees. Defined benefit pensions/OPS were discontinued for employees joining after April 1, 2004.

- Eligibility: Any individual citizen of India (both resident and non-resident) in the age group of 18-70 years can join NPS.

- Multiple Accounts: Opening multiple NPS accounts for an individual is not allowed under NPS.

This information provides a clear distinction between the Old Pension Scheme and the National Pension Scheme, highlighting their key features and eligibility criteria.

Nirbhaya Fund:

- Introduction: Introduced by the Centre in 2013 to assist women in distress, improve infrastructure and manpower for their support, and create safer environments.

- Fund Allocation: It is a non-lapsable corpus fund of Rs 1000 crores provided by the Centre, utilized by states to ensure women’s safety.

- Nodal Agency for Fund Administration: Department of Economic Affairs under the Ministry of Finance.

- Nodal Agency for Expenditure: Women and Child Development (WCD) Ministry.

- Schemes Implemented by WCD under Nirbhaya Fund:

- One Stop Centre

- Universalisation of Women Helpline

- Mahila Police Volunteer

- Schemes Implemented by the Home Ministry under the Nirbhaya Fund:

- Emergency Response Support System

- Central Victim Compensation Fund

This fund plays a crucial role in supporting initiatives and programs that aim to enhance the safety and well-being of women in India.

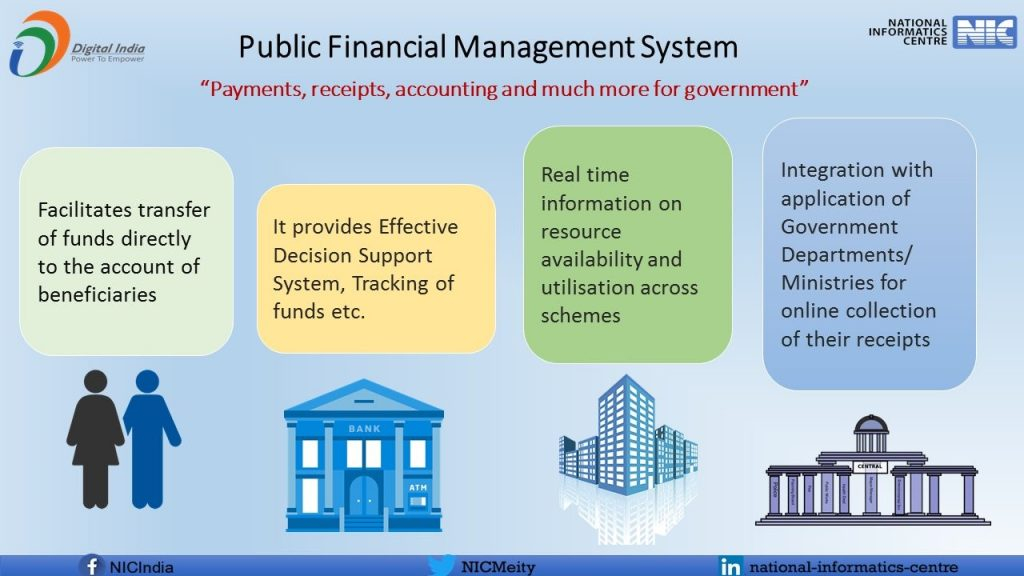

Public Financial Management System (PFMS):

- Overview: An online platform developed by the office of the Controller General of Accounts (CGA) under the Union Ministry of Finance. It facilitates direct payments to beneficiaries of government schemes.

- History: Initially launched in 2008-09 as a pilot scheme named CPSMS in four states. It started with four flagship schemes – MGNREGS, NRHM, SSA, and PMGSY. In December 2013, it was approved for national rollout to all states.

- Mandate:

- Acts as a financial management platform for plan schemes.

- Enables efficient tracking of fund flow to the lowest level of implementation.

- Provides information on fund utilization for better monitoring and decision support.

- Achievements:

- Transformed Direct Beneficiary Transfers in Financial Governance.

- Handled around 102 crore DBT transactions in FY 19-20, totalling about ₹2.67 lakh crore.

- Estimated to have saved about ₹1 lakh crore through efficient technology use.

Factors for the Successful Evolution of PFMS:

- Onboarding/Integrating all Govt. Accounts: Ensuring significant coverage for effective execution.

- Data Management Capabilities: Enhancing data management for better monitoring and review.

- Continuous Upgradation: Adapting to rapid technological changes with a focus on upgradation and monitoring.

- Collaboration with Banking System: Integration with banking systems is critical for successful execution.

PAC Observations:

- Concerns:

- PAC expressed concern about data security of PFMS.

- Highlighted the need for a dedicated workforce and strategic measures to address evolving technological threats.

- Infrastructure Assessment: Emphasized the necessity for a thorough evaluation of physical and technical infrastructure, including backup arrangements.

Conclusion:

- PFMS has revolutionized public finance management in India and continues to evolve with improvements and increasing coverage. Continuous efforts are required to address concerns and ensure the system’s effectiveness.

This comprehensive summary provides a clear overview of the PFMS and the considerations raised by the PAC.

The Atal Pension Yojana (APY)

It is a social security scheme launched in 2015 with the aim of providing a universal social security system for all Indians, with a special focus on those in the unorganized sector. Here are some key details about APY:

- Objective: The scheme is focused on creating a social security net, especially for the poor, underprivileged, and workers in the unorganized sector.

- Eligibility:

- Individuals must be bank account holders in the age group of 18 to 40 years to be eligible for APY.

- Subscribers can enroll in APY through a bank branch, post office, or online/offline modes.

- Contributions:

- Subscribers can make contributions on a monthly, quarterly, or half-yearly basis through automatic debit from their savings bank accounts.

- Benefits:

- After reaching the age of 60, subscribers are entitled to receive a minimum monthly pension ranging from Rs. 1000 to Rs. 5000.

- In case of the subscriber’s demise, their spouse is guaranteed a pension for life.

- Government Co-contribution:

- The government co-contributes 50% of the subscriber’s contribution or Rs. 1000 per annum, whichever is lower. This is applicable to eligible subscribers who joined the scheme between 1st June 2015 and 31st March 2016, and who are not beneficiaries of any other social security scheme and are not income taxpayers.

- Nodal Agency:

- The scheme is administered by the Pension Fund Regulatory and Development Authority (PFRDA), a statutory authority under the Ministry of Finance. PFRDA also oversees the National Pension System (NPS).

- Restrictions:

- Subscribers are not allowed to hold multiple APY accounts.

- Recent Update:

- As of October 1, 2022, income taxpayers are no longer eligible to join the APY scheme as per the guidelines of the Finance Ministry.

With over 2 crore subscribers, APY plays a crucial role in providing financial security to individuals in the unorganized sector, especially during their retirement years.

FAQs

Q1. What is the role of the Ministry of Finance?

The Ministry of Finance plays a pivotal role in formulating and implementing economic policies, managing public finances, and overseeing financial regulations. We are dedicated to fostering economic growth, maintaining fiscal stability, and ensuring responsible use of resources.

Q2. How does the Ministry of Finance contribute to economic development?

We contribute to economic development through strategic planning, budget allocation, and policy implementation. By promoting investment, managing public debt, and fostering a conducive business environment, we aim to drive sustainable growth and prosperity.

Q3. What measures does the Ministry of Finance take to ensure fiscal responsibility?

Fiscal responsibility is paramount to us. We implement prudent fiscal policies, monitor expenditure, and optimize revenue collection. Additionally, we prioritize transparency and accountability in financial management to uphold the public trust.

Q4. How does the Ministry of Finance support citizens’ financial well-being?

We support citizens’ financial well-being by designing policies that promote inclusive growth and equitable distribution of resources. From social welfare programs to tax reforms aimed at relieving burdens on low-income individuals, our initiatives aim to improve the financial resilience of all citizens.

Q5. What initiatives is the Ministry of Finance undertaking to address economic challenges?

We are constantly adapting to address economic challenges. Our initiatives may include stimulus packages during economic downturns, reforms to enhance competitiveness, and investments in key sectors such as infrastructure and education. Through proactive measures and collaboration with stakeholders, we strive to navigate economic uncertainties and foster resilience.

In case you still have your doubts, contact us on 9811333901.

For UPSC Prelims Resources, Click here

For Daily Updates and Study Material:

Join our Telegram Channel – Edukemy for IAS

- 1. Learn through Videos – here

- 2. Be Exam Ready by Practicing Daily MCQs – here

- 3. Daily Newsletter – Get all your Current Affairs Covered – here

- 4. Mains Answer Writing Practice – here